The global foreign exchange market

functions as the primary circulatory system for international finance, boasting

a daily turnover that currently averages $7.5 trillion. But for the

individual trader, accessing this vast, decentralized landscape requires a

specific intermediary. So, what is a forex broker exactly?

At its core, a retail forex broker

acts as the essential conduit, providing individual and intermediate-level

participants with the infrastructure necessary to interact with a market

historically dominated by massive institutional players. However, understanding

what a forex broker is requires more than a simple definition; it demands a

multi-layered analysis of their business models, technological stacks, and the

increasingly sophisticated role of artificial intelligence in both trading and

education.

This report provides an exhaustive

investigation into the mechanisms that drive modern brokerage operations,

answering the fundamental question of "what acts behind the buy and sell

buttons" by exploring revenue models and the structural evolution from

traditional dealing desks to AI-augmented execution hubs.

To

comprehend the retail layer, one must first identify the foundation upon which

it sits: the wholesale interbank market. Unlike traditional stock exchanges,

the foreign exchange market is an over-the-counter (OTC) environment

characterized by a two-tier market structure.

The

first tier is the inter-dealer market, which operates across multiple

high-speed trading venues and electronic communication networks (ECNs). Access

to this inner sanctum is strictly limited to dealer banks and the clients of

prime broker banks. These "Tier 1" liquidity providers—including

global giants such as JPMorgan, Deutsche Bank, Citi, and UBS—possess the market

capitalization and technological infrastructure to provide the deepest

liquidity and tightest spreads.

The

role of liquidity providers in forex brokerage is to maintain market depth and

ensure that large orders can be executed without causing significant price

disruptions. While Tier 1 banks dominate the market, Tier 2 and Tier 3

providers, such as regional banks and specialized hedge funds, play a vital

complementary role by offering liquidity for less liquid or "exotic"

currency pairs. Retail brokers aggregate these various price streams through a

liquidity bridge or a "Prime of Prime" relationship, effectively

translating wholesale market conditions into retail-friendly formats.

In

this ecosystem, prime brokers serve as the ultimate credit intermediaries.

Because the interbank market is a credit-approved system, institutions only

trade with counterparties for whom they have established credit relationships.

Retail brokers often lack the balance sheet to trade directly with a dozen Tier

1 banks. Consequently, they utilize "Prime of Prime" firms that

aggregate liquidity from multiple tier-1 sources and redistribute it to smaller

operators. This aggregation process is critical; it allows the broker to stream

the "Best Bid and Ask" (BBO) prices to their clients, narrowing the

spread by selecting the tightest prices available from across their provider

network.

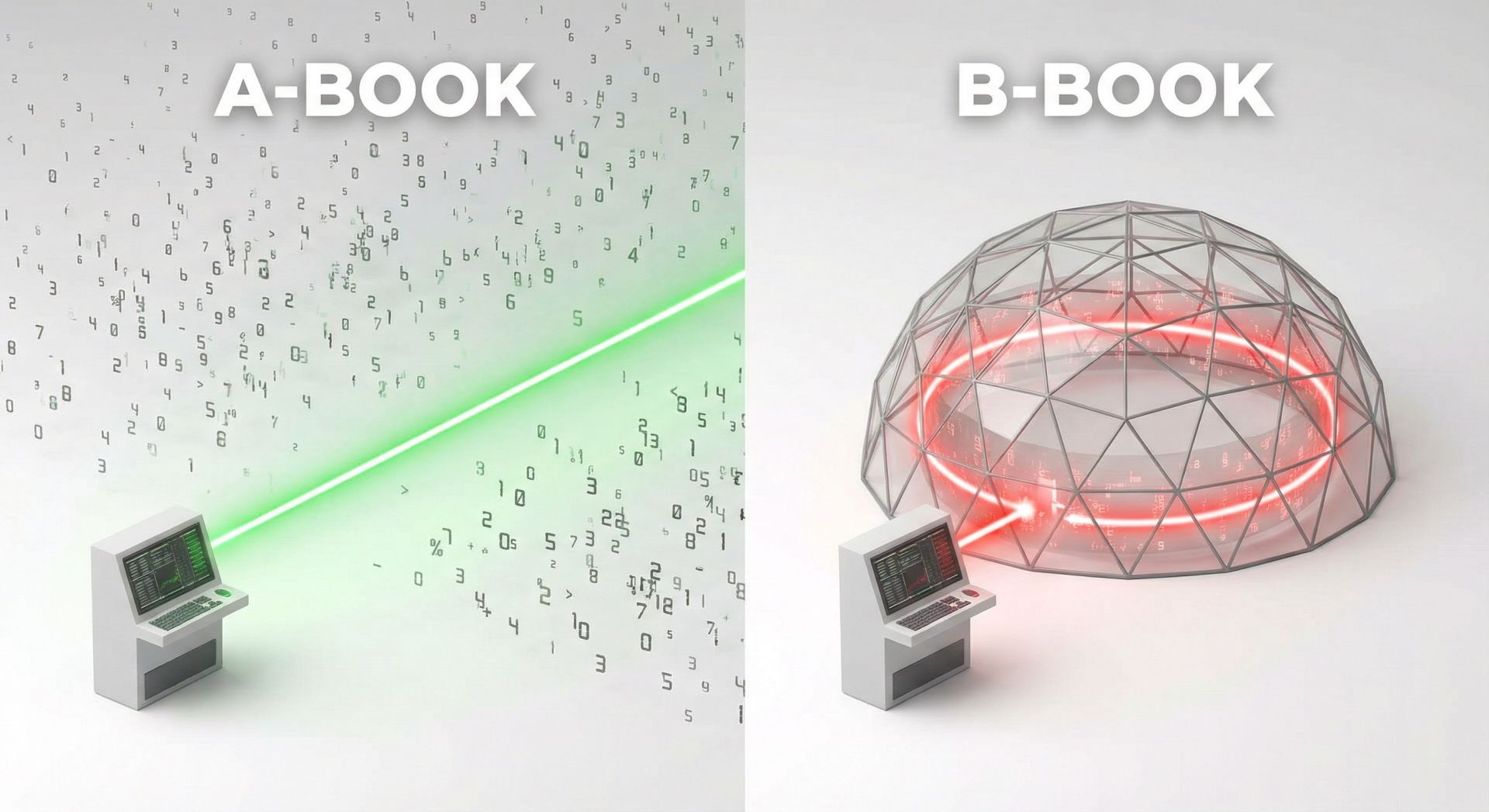

A

central component of the brokerage industry is the internal management of

client order flow, commonly divided into the A-Book and B-Book models. These

models define the broker's risk management strategy and dictate their profit

motives.

An

A-Book broker operates under an agency model, functioning as a bridge between

the trader and external liquidity providers. When a client places a trade, the

broker instantly "mirrors" that trade with a bank or an ECN.

|

Aspect

|

A-Book

Broker (STP/ECN)

|

|

Execution

Reality

|

Pass trades to

the external market

|

|

Revenue

Model

|

Transparent

commissions and small spread markups

|

|

Conflict

of Interest

|

Low; the broker

benefits from client success and volume

|

|

Typical

Users

|

Active traders,

scalpers, and institutional clients.

|

The

primary advantage of this model is the elimination of the direct conflict of

interest. Since the broker makes money through volume-based fees, they are

incentivized to provide high-quality execution and tools that help their

clients stay profitable over the long term.

Conversely,

B-Book brokers operate as market makers. These firms internalize their clients'

trades, meaning the orders never leave the broker's own internal system. In

this scenario, the broker acts as the counterparty—if the trader buys, the

broker sells to them from their own inventory.

The

revenue model for a market maker is derived from the spread and, importantly,

from net client losses. While this creates a potential conflict of interest,

the model provides specific benefits to certain classes of traders. Because the

broker controls the environment, they can offer "instant" fills on

small orders, fixed spreads, and access to trading with very low minimum

deposits. For beginners, the simplicity and predictability of a B-Book broker

can be an advantage, provided the broker is reputable and well-regulated.

Most

sophisticated modern brokers utilize a hybrid model. Using advanced algorithms

and behavioral analysis, the broker categorizes traders into different

"books". Profitable, high-volume traders are typically A-Booked to

protect the broker from significant payouts, while less experienced or

consistently losing traders are kept in the B-Book.

Some

brokers also utilize a "C-Book" strategy, where they selectively

hedge only the net exposure of a group of traders rather than individual

positions. This dynamic management allows the broker to maximize its

efficiency, taking on market risk when statistically favorable and passing it

to external providers when exposure reaches certain risk thresholds.

Understanding

how forex brokers make money requires looking beyond the "zero

commission" marketing claims often seen in the industry. Brokers utilize a

combination of spreads, markups, commissions, and financing fees to maintain

their operations.

The

most universal source of revenue is the bid-ask spread. The 'bid' is the price

at which the broker is willing to buy a currency from you, and the 'ask' is the

price at which they are willing to sell it to you.

Brokers

calculate their spreads by taking the raw interbank rates and adding a

"markup". For example, if the interbank EUR/USD spread is 0.1 pips, a

broker might add a 0.5 pip markup, presenting a 0.6 pip spread to the end-user.

This markup represents the broker's "fee" for facilitating the trade.

Traders must choose between fixed and variable spreads. Fixed spreads remain constant regardless of market conditions and are typically offered by market makers to provide cost predictability. Variable spreads, offered by ECN and STP brokers, fluctuate based on real-time market liquidity and volatility. While variable spreads are often much tighter during high-liquidity sessions (like the

London-New York overlap), they can widen dramatically during news events or periods of extreme volatility.

How do zero spread forex brokers work? These brokers typically offer "raw" spreads directly from liquidity providers, which can be as low as 0.0 pips on major pairs. However, they recoup their costs by charging a fixed "commission per lot". This structure is favored by high-frequency traders and scalpers because it provides greater price transparency and often a lower total transaction cost for high-volume strategies.

Why

do forex brokers charge swaps? Forex trades are technically spot transactions

that settle in two days (T+2). If a position is held past the daily

"roll" time (usually 5:00 PM EST), it must be rolled over to the next

value date. This involves paying or receiving interest based on the

differential between the two currencies in the pair. Brokers typically add a

markup to these interest rate differentials, turning the "swap" into

another source of revenue.

The

point-based swap formula is calculated as:

How does leverage work in forex trading? It is essentially the use of "borrowed" capital to increase a trader's buying power. Leverage allows a participant to control a large position with a relatively small amount of equity, which is known as "trading on margin".

How

do brokers calculate margin requirements? Margin is not a cost, but a

"good-faith deposit" held by the broker to cover potential losses. It

is usually expressed as a percentage of the total notional value of the trade.

|

Instrument

|

Leverage

Ratio

|

Margin

Requirement

|

|

Major

Pairs

|

30:1

|

3.33%

|

|

Minor

Pairs / Gold

|

20:1

|

5.00%

|

|

Commodities

|

10:1

|

10.00%

|

|

Cryptocurrencies

|

2:1

|

50.00%.

|

The

formula for required margin is:

Brokers

use automated monitoring to ensure accounts remain sufficiently funded. The

"Margin Level" is the ratio of equity to used margin:

$$\text{Margin

Level} = \left( \frac{\text{Equity}}{\text{Used Margin}} \right) \times 100$$

.

If

the margin level drops below a specific threshold (often 100%), the broker may

issue a "margin call," prohibiting new trades. If it hits the

"stop-out" level (typically 50%), the broker is legally required in

many jurisdictions to liquidate open positions to prevent the account from

falling into a negative balance.

In the competitive world of currency trading, execution speed is a primary metric of broker quality. "Latency" refers to the time delay between a trader placing an order and the broker's system executing it.

While

a standard home internet connection might result in execution speeds of 50ms to

200ms, "low-latency" trading focuses on sub-1ms speeds. Ultra-low

latency environments, often used by high-frequency traders, push these

boundaries into the microsecond range.

|

Setup

Quality

|

Latency

Range

|

Impact

on Slippage

|

|

Premium

(Colocated)

|

0.3ms - 1ms

|

Near-zero

slippage; optimal for HFT.

|

|

Optimized

(VPS)

|

5ms - 20ms

|

Low slippage;

excellent for EAs.

|

|

Standard

(Home)

|

50ms - 150ms

|

Noticeable

slippage during volatility.

|

Physical

distance plays a massive role in execution speed. Data travels through fiber

optic cables at roughly 200,000 km/second, meaning every kilometer adds

approximately 4.9 microseconds of delay. This physical reality explains why

many brokers colocate their servers in the same buildings as their liquidity

providers, such as the Equinix data centers in London (LD4) and New York (NY4).

Why

do forex spreads widen during news? This phenomenon is primarily due to

"liquidity withdrawal". During major economic releases (like interest

rate decisions), the uncertainty is so high that tier-1 banks and other

liquidity providers may temporarily pull their quotes or widen their own

spreads to mitigate risk. Brokers, who rely on these providers for pricing,

must widen the spreads seen by retail clients to avoid being left with

un-hedged, losing positions in a rapidly shifting market.

A central piece of the puzzle is the "bridge," a sophisticated piece of software that facilitates communication between the retail trading platform and the institutional market.

What

is the role of a bridge in forex trading? Most retail platforms, like

MetaTrader 4 or MT5, were not originally designed to connect to multiple

external liquidity pools simultaneously. The bridge acts as a translator, using

FIX API protocols to send trade data between the broker's server and the liquidity

provider's execution engine. It allows for real-time risk management, automated

A/B book routing, and price aggregation.

While

MetaTrader 4 remains the industry standard for its massive library of Expert Advisors

(EAs), MetaTrader 5 offers more advanced capabilities for multi-asset trading

and faster backtesting. cTrader, another popular alternative, is often favored

for its "Direct Market Access" (DMA) feel and high-tier charting

tools.

The

life of a forex trade is a sequence of highly coordinated digital events that

take place in a fraction of a second.

- Order Initiation:

The trader selects a pair, size, and direction on their platform.

- Platform Validation:

The broker's server confirms the trader has enough margin to open the

position.

- Bridge Processing:

The bridge evaluates the trade based on the broker's risk rules—deciding

if the broker will take the other side (B-Book) or pass it to an LP (A-Book).

- Execution:

If A-Booked, the bridge sends a FIX message to the liquidity provider with

the best current price. If B-Booked, the broker instantly fills the order

against their internal book.

- Confirmation:

The execution report travels back to the trader's terminal, updating their

"Open Positions" and balance.

The

convergence of forex education and AI is reshaping how new participants learn

the market. AI is moving beyond simple automation into the realm of

"experimental learning" and behavioral coaching.

AI

platforms are being used to create "flight simulators" for traders.

Unlike traditional demo accounts, these AI-driven simulations use tick-level

historical data to replicate exact market conditions, including spreads and

slippage.

One

of the most advanced applications is "Mentor AI," which acts as a

personal strategy coach. Instead of just recording trades, the AI analyzes a

trader's behavior to identify recurring mistakes, such as "revenge

trading" or poor risk-reward ratios. This creates a "feedback

loop" that allows beginners to refine their strategies based on data

rather than emotion. Intermediate traders seeking to optimize their workflow

can explore a dedicated at the following to see these systems in practice.

On

the institutional side, AI risk management systems act as "financial

bodyguards". They monitor positions 24/7, calculating correlations between

seemingly different pairs to ensure that a trader isn't unknowingly

over-exposed to a single underlying economic factor. For algorithmic traders,

AI tools like Long Short-Term Memory (LSTM) networks are being used to forecast

short-term price movements with high directional accuracy, enabling more

precise entry and exit points.

A

paramount concern for any trader is the safety of their capital. This safety is

primarily determined by the regulatory oversight of the chosen broker.

The

most respected regulatory bodies include the Financial Conduct Authority (FCA)

in the UK, the Australian Securities and Investments Commission (ASIC), and the

Cyprus Securities and Exchange Commission (CySEC).

These

regulators impose strict requirements:

- Segregated Accounts:

Brokers must keep client funds in bank accounts separate from the broker's

own operational funds, ensuring that client money cannot be used to pay

company debts.

- Capital Adequacy:

Brokers must maintain a significant capital buffer (e.g., £730,000 for FCA

market makers) to ensure they can weather market volatility.

- Compensation Schemes:

In the event of broker insolvency, schemes like the FSCS (UK) or ICF

(Cyprus) protect client funds up to a certain limit (e.g., £85,000 or

€20,000).

To

maintain their licenses, brokers must perform rigorous "Know Your

Customer" (KYC) and "Anti-Money Laundering" (AML) procedures.

While these checks can be time-consuming for the trader, they are essential for

preventing fraud and ensuring the integrity of the wholesale FX market.

Counterparty risk is the danger that the broker (the other "party" to

your trade) might fail to fulfill its obligations. Choosing a broker with

tier-1 regulation and a transparent "A-Book" preference significantly

mitigates this risk.